Having retirement savings through a 401(k) or IRA will replace your bi-weekly salary when you decide to retire and will help you pay for everything you need and want to do in life, including going on vacation, paying medical expenses, dining out, vehicle and housing costs, and more.

Saving for retirement is an essential part of financial planning, but it’s easier said than done. If you’re concerned about having enough money to live on in your golden years, read our tips below for simple ways to amplify your savings for the future.

Get the Most Out of Your Employer’s 401(k) Program

Enrolling in your employer’s 401(k) plan is a great way to help you save for retirement and is step #1 to getting started. These accounts are often managed by a financial planner or company who oversees the entirety of staff accounts, educating you to make confident decisions for your financial future.

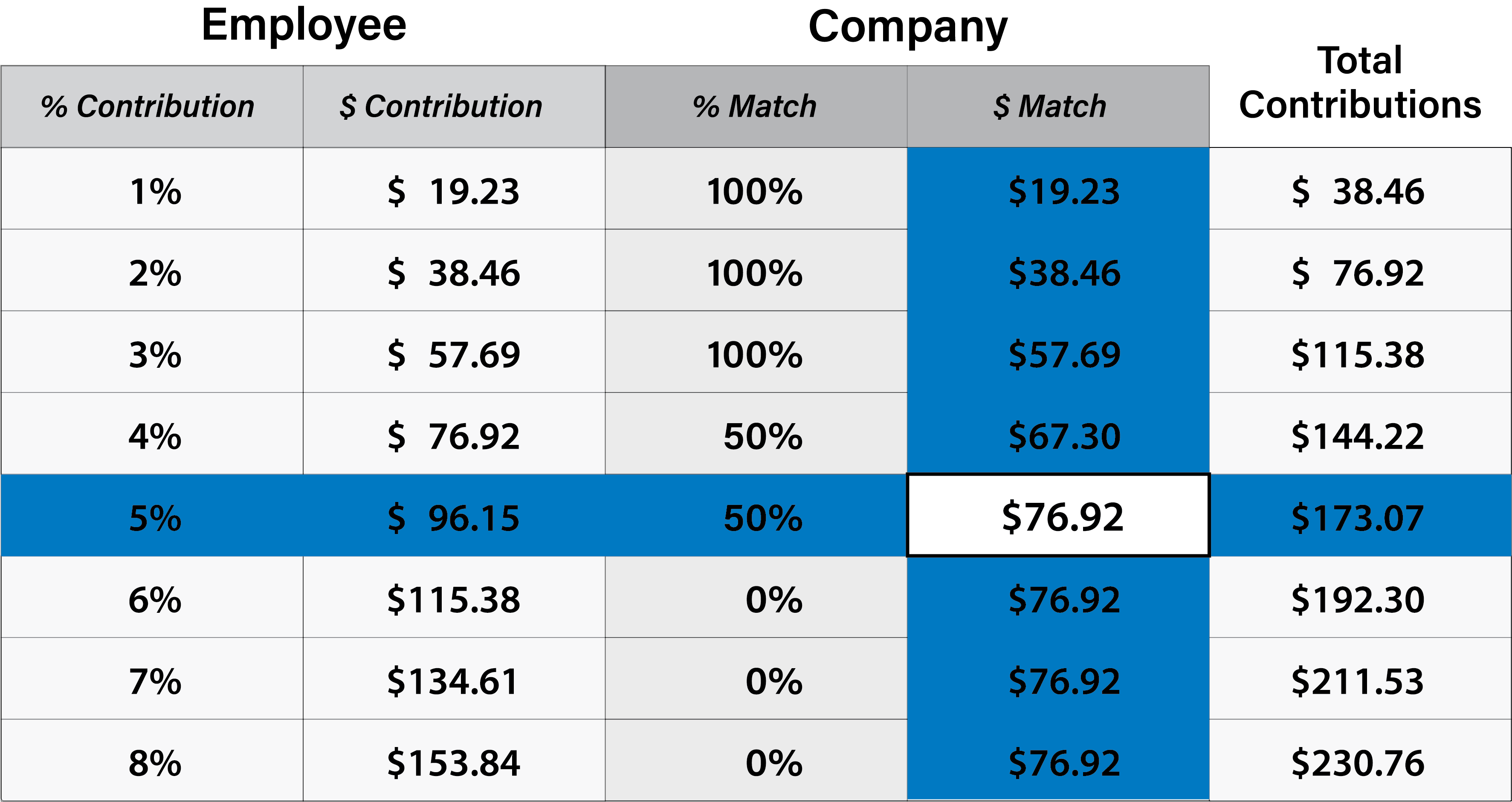

In addition to plan management, your employer may also offer a 401(k)-matching program, which allows you to boost your retirement savings alongside your employer. A match program allows both you and the employer to make contributions to your retirement account, though there is typically a cap on how much your employer will match.

For example, if you work for a company with a 5% match rule, then they will match up to 5% of your contributions to your account, meaning that your annual 5% contribution is now 10%. Regardless of how the matching contribution plan is structured, if there’s free money available, take advantage!

What Are the Employer Match Requirements?

Companies with a match program often require length of employment minimums to ensure they don’t lose money if you decide to leave the company early. In this instance, an employee who utilizes the match will have to work with the company for a specific number of years, typically between two and five years. If the employment is terminated for any reason before that designated period, then the employer can withdraw their contributions from the account.

If you’re not sure if your employer offers a 401(k) match, reach out to the human resources team or benefits specialist for assistance. Together, they can help you determine eligibility, term minimums, contribution amounts, and other important information for the plan.

You can learn more about the benefits of enrolling in your employer’s 401(k) on the Slavic401k blog.

Budget with the 50/30/20 Rule

If putting additional funds into a 401(k) isn’t an option for you right now, the next best thing is to create or revise your budget. The 50/30/20 rule is a simple method for budgeting monthly net income into three major categories: 50% for needs, 30% for wants, and 20% for savings and debt payoff.

Mobile apps like Mint, PocketGuard, or You Need a Budget (YNAB), can help you visualize your categories to ensure that you’re living within your means. These apps allow you to connect your debit and credit cards, loans, bank accounts, and retirement accounts to help you set savings and debt payoff goals, pay bills, and categorize transactions – all at your fingertips!

The apps also allow you to visualize where you may be overspending, such as the wants and desires category, which includes non-essential spending like dining out, going on vacation, or monthly subscription services. If you see that happening, you can adjust your budgets within the app to ensure you have extra money to contribute to savings each month.

These small steps can make a big impact on your future finances by making financial management easy and stress-free. Plus, with a budget that’s in your pocket at all times, you’re sure to hold yourself accountable (plus, there are notifications that will remind you when you are nearing your spending limits)!

Open a Health Savings Account

Healthcare costs can add up, especially as you get older. Increased costs of medications and services require cash up-front to pay for care, so having an account like a Health Savings Account (HSA) can help you plan for future expenses without tapping into your retirement savings.

The Internal Revenue Service (IRS) determines individual and family plan contribution limits each year, which allows participants to put money aside for medical expenses.

The contributions to the plan are 100% tax-deductible and can be used for medical expenses over time and when a participant reaches 65 years of age, the funds within the plan can be used outside of medical-related costs as well, according to Mark Hebner of Index Funds Advisors.

Because of this, investors can use their HSA as a secondary retirement account, which can assist with medical and non-medical related expenses during the golden years.

Read on blog, Using A Health Savings Account: What You Need to Know, for in depth information on HSAs.

Contribute Tax Refunds, Raises, Bonuses, and Extra Cash

In addition to budgeting, enrolling in your employer’s 401(k) match, and opening an HSA, you can also plan to save any additional funds you make throughout the year to your retirement savings. Extra funds can include raises and bonuses, gift money, tax refunds, or cash earned from a side hustle.

These additional savings can add up over time, allowing you to invest more aggressively or put funds away for the future.

Saving money for retirement may not come easy to everyone, but with the proper steps and guidance, anyone can prepare for the future. Calculators like Slavic401k’s retirement planner, can help you determine how much money you’ll need for retirement and will help you in adjusting your budget, savings, and spending over time.

Questions? Visit slavicwealth.com to speak with a financial advisor.