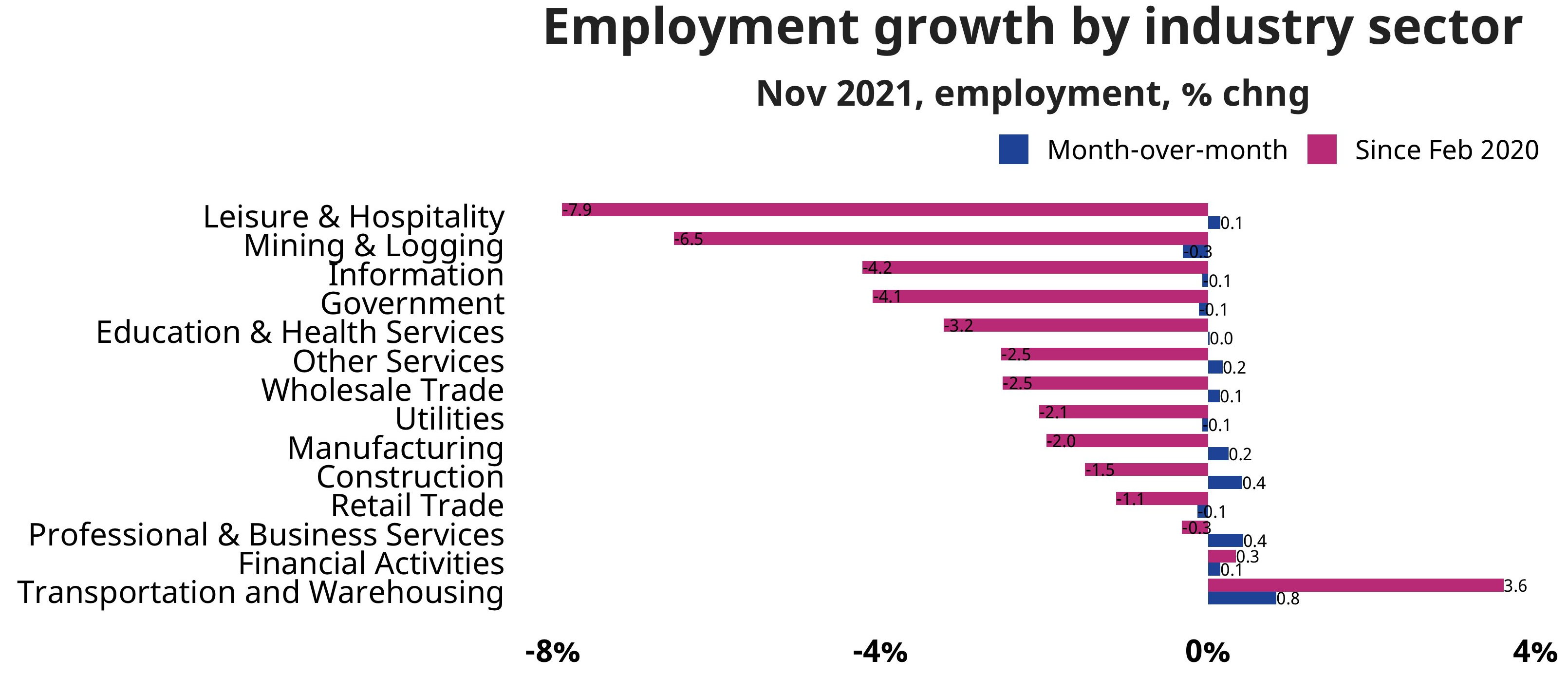

The latest monthly job report from the U.S. Labor Department revealed that nonfarm payrolls growth slowed in November, with “only” 210,000 jobs being added back to the economy.

That was less than half the gain expected and the smallest monthly increase this year. There was a net upward revision of 82,000 payrolls to the September and October reports, although this still resulted in a 3-month average gain of just of 378,000, the weakest reading since February. At that pace of job creation and with total employment in America remaining 3.9 million payrolls below the pre-crisis peak, an arguably conservative estimate, it would still take roughly another 10 months to completely erase the pandemic-related jobs deficit.

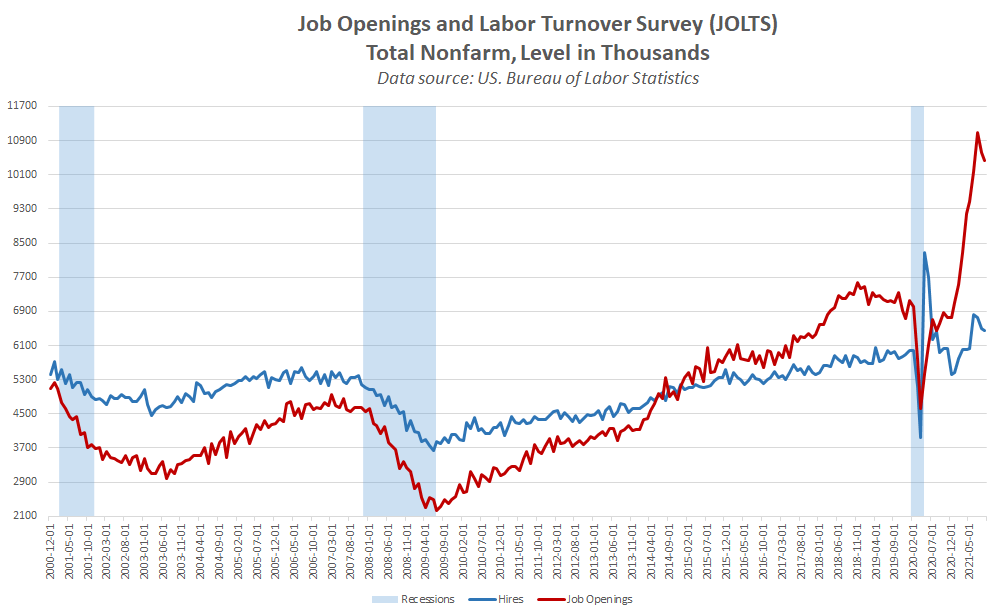

In the near-term a combination of winter weather and the uncertainty around new COVID variants may further dampen hiring (and overall economic activity) but as these headwinds start to fade it is easy to see payrolls growth firming again in 2022, especially once the services sector hiring reacceleration resumes, in turn potentially erasing the jobs deficit quicker. More importantly, regardless of how one wants to interpret November’s noisy payrolls report, there is little doubt that it could have been stronger if the supply of workers was better. Put another way, demand has definitely not been a headwind for job growth this cycle because openings have exceeded hires by an average of 47 percent this year, and 62 percent as of the latest (September) JOLTS data from the U.S. Labor Department.

Similarly, initial claims for unemployment benefits continue to hover near the lowest level of the recovery and suggest employers remain reluctant to let workers go due to a lack of confidence that vacant positions can be quickly filled. This is even a problem for large businesses, as evidenced by the latest Challenger data that showed there were 14,875 corporate layoffs in America in November, the lowest reading since 1993. Moreover, large employers year-to-date have announced plans to cut 302,918 jobs from their payrolls, down 86 percent when compared to the first 11 months of 2020 and the lowest January-November total on record. “Company closings” were cited as the most common reason for announced job cuts this year, followed closely by “restructuring,” again confirming that layoffs are typically only occurring when no other option is available.

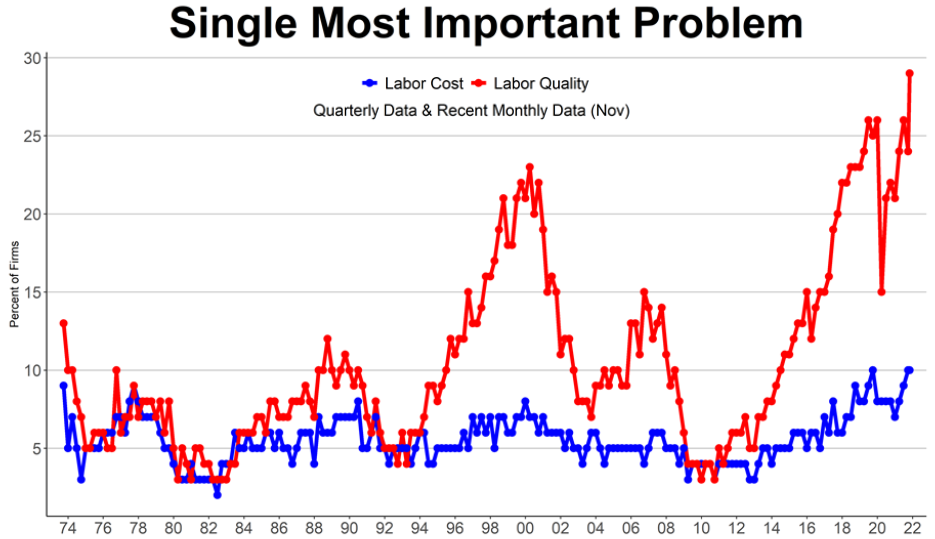

This dynamic could have an interesting effect on seasonal trends where instead of employers shedding extra workers after the holidays they instead try to get ahead of future labor shortages by holding onto the seasonal workers and locking in higher employment. Smaller businesses are even more likely to take this approach because the latest NFIB survey revealed that nearly a third (29 percent) of small business owners in November cited labor quality as the top problem their company is facing at the moment, a half-century high. Forty-four percent of small firms boosted pay last month, another multi-decade high. If pay raises are helping, though, the benefit has so far been minimal because some 48 percent of surveyed owners reported having job openings they could not fill recently, the second monthly decline in a row but historically still extremely high.

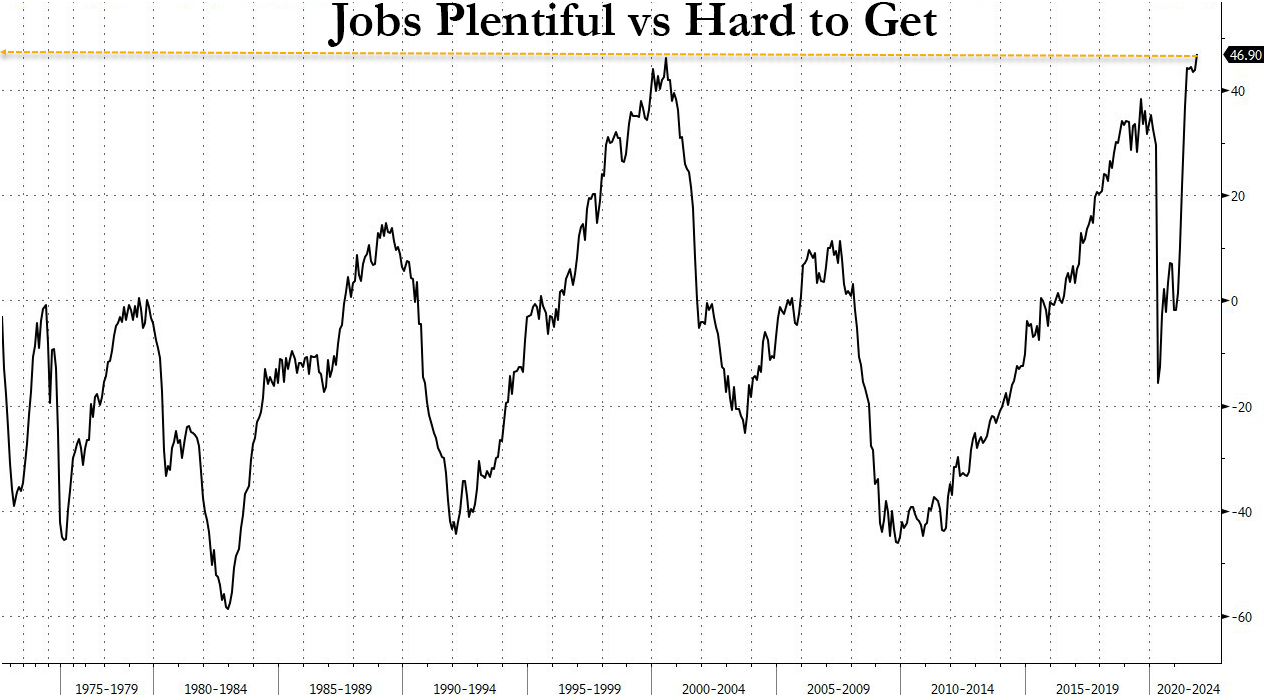

A relatively smaller percentage of surveyed owners cited labor costs as their top problem, although at 10 percent it is still at the high end of the historical range. One could argue that this means pricing power remains strong for most small businesses, which could clear the way for more wage gains in the months ahead. Such conditions have not gone unnoticed by working Americans because the latest consumer confidence survey conducted by The Conference Board revealed that labor market optimism has never been higher. Specifically, the proportion of respondents who believe jobs are “plentiful” exceeded those who feel jobs are “hard to get” by the widest margin on record last month, and optimism about future earnings power remained elevated as well.

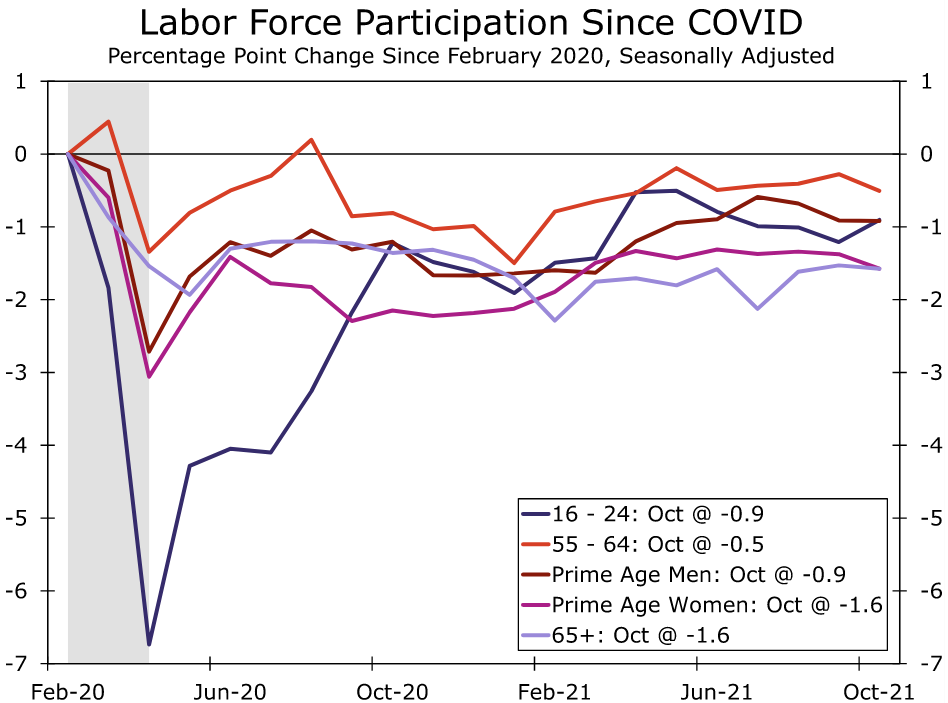

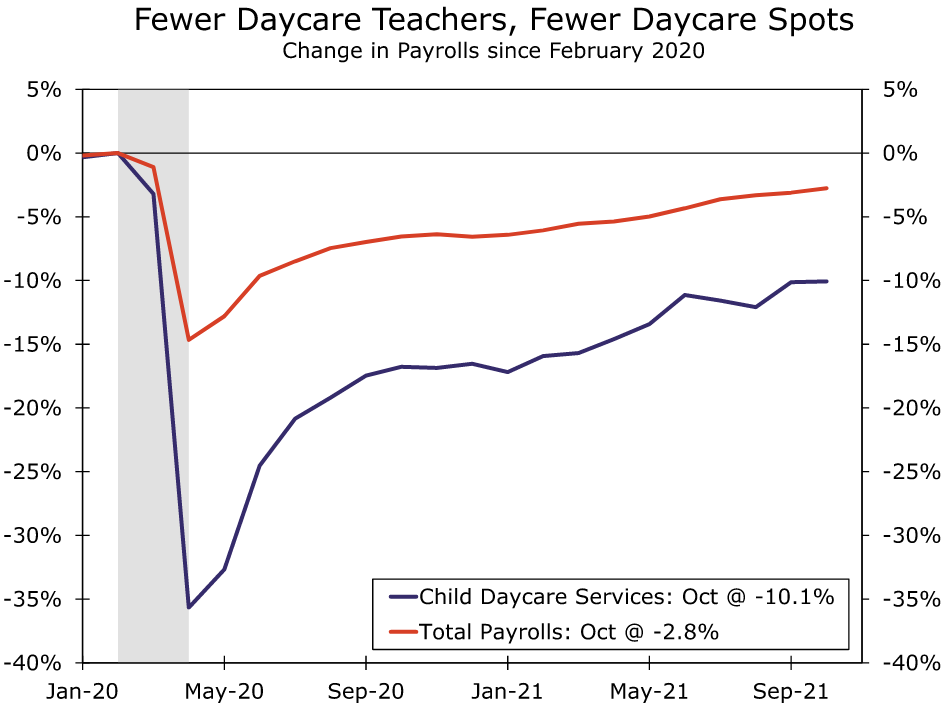

Another problem for employers is that the labor supply has not just been hurt by increases in worker confidence (bargaining power) but also lingering effects from the pandemic. Seniors (65+), for instance, have accounted for nearly a quarter of the “missing” workers this crisis despite comprising just 7 of the workforce (pre-COVID). While people can “un-retire,” the likelihood of transitioning back to employment from retirement has historically been quite low. Prime-age (25-54) women may therefore be a better avenue for employers to explore when trying to fill vacancies in this market because labor force participation in this cohort remains severely depressed but the probability of this group returning to the workforce is much higher than for senior retirees. Near-term headwinds, however, include childcare challenges that could persist through the winter months and perhaps even longer while daycare centers continue to struggle to hire.

What To Watch This Week:

Monday

- Nothing significant scheduled

Tuesday

- International Trade in Goods and Services 8:30 AM ET

- Productivity and Costs 8:30 AM ET

- 3-Yr Note Auction 1:00 PM ET

- Consumer Credit 3:00 PM ET

Wednesday

- MBA Mortgage Applications 7:00 AM ET

- JOLTS 10:00 AM ET

- EIA Petroleum Status Report 10:30 AM ET

- 10-Yr Note Auction 1:00 PM ET

Thursday

- Jobless Claims 8:30 AM ET

- Wholesale Inventories (Preliminary) 10:00 AM ET

- EIA Natural Gas Report 10:30 AM ET

- 30-Yr Bond Auction 1:00 PM ET

- Fed Balance Sheet 4:30 PM ET

Friday

- CPI 8:30 AM ET

- Consumer Sentiment 10:00 AM ET

- Quarterly Services Survey 10:00 AM ET