In recent years, interest rates have become a major topic in the financial sector. The Federal Reserve steadily increased rates to combat inflation, with rates now beginning to slowly fall again. It’s important to understand how these changes can impact your retirement savings.

While higher rates can offer some benefits, they can also pose challenges to those trying to build wealth for the future. We explain how interest rates affect different aspects of retirement planning and what you can do to navigate these changes.

Understanding Interest Rates and Federal Fund Rate

Interest Rates

This is the cost of borrowing money or the return earned on savings. They directly influence the cost of loans (like mortgages or car loans) and the earnings from savings accounts. These affect how much things cost and how much people spend.

Federal Funds Rates

This is a special interest rate that banks charge each other for overnight loans to meet the reserve requirements. It serves as a benchmark for many other interest rates, such as those for credit cards, home loans, and business loans.

Role of the Federal Reserve

The Federal Reserve (the Fed) sets a target range for the federal funds rate to help steer the economy. Adjusting this rate influences borrowing and spending. A lower rate makes borrowing cheaper, encouraging spending and investment, while a higher rate makes borrowing more expensive, helping to control inflation. Changes in the federal funds rate create a ripple effect on borrowing costs throughout the economy.

1. Impact on Savings Accounts and CDs

One of the most immediate effects of changing interest rates is on savings accounts and Certificates of Deposit (CDs). When the Federal Reserve increases interest rates, banks usually offer higher interest rates on savings accounts and Certificates of Deposit (CDs). This means you can earn more money on your savings. So, if you’re saving money for a short time, it’s a good opportunity to get better returns on your savings.

Pros for Retirement Savers:

- Higher Rates Often Mean Higher Yields: If you have funds in a high-yield savings account or CDs, you may see an increase in interest earnings. In an economy where rates are high, some savers might opt for the security of cash-like products that now offer better returns. For retirees who rely on stable, low-risk income streams, this can be a welcome change.

- Locking in Rates: If you anticipate rates dropping, locking in a CD at the current rate might be beneficial. However, if rates rise, you might want to consider shorter-term CDs or wait for better rates. Keep an eye on rate trends and adjust your savings strategy accordingly.

Cons for Retirement Savers:

- Reduced Buying Power: While your savings might grow more quickly when rates are high, the rising cost of goods due to inflation could erode your purchasing power, especially for those relying solely on interest income for retirement.

- Opportunity Cost: By focusing on safe, high-interest products, you might miss out on the potential higher returns offered by stocks or bonds, which are vital for long-term wealth growth.

2. Impact on Bonds

Bonds, often a cornerstone of retirement portfolios, are highly sensitive to interest rate changes. Bond prices and interest rates have an inverse relationship because existing bonds with higher interest rates become more attractive compared to new bonds issued at lower rates.

How This Affects You:

Existing Bonds:

- If Interest Rates Go Up: The value of your current bonds will likely go down. This is because new bonds will be issued with higher interest rates, making your older bonds less attractive. This is especially the case for long-term bonds, which are more vulnerable to rate increases.

- If Interest Rates Go Down: The value of your current bonds will likely go up. Low interest rates can increase the demand for bonds as investors seek safer investments with predictable returns. If you already own bonds, this increase in price can boost the value of your investment.

New Bonds:

- If Interest Rates Go Up: On the flip side, new bonds issued after a rate hike will offer higher yields, making them more attractive for those who are purchasing bonds in the current environment.

- If Interest Rates Go Down: These will offer lower yields, meaning the return on investment will be less compared to bonds issued when interest rates were higher.

What You Can Do:

- Diversify Your Bond Holdings: To mitigate risk, investors might want to consider diversifying your bond portfolio by including a mix of short- and long-term bonds.

- Consider Treasury Inflation-Protected Securities (TIPS): These government bonds are designed to protect against inflation, making them an ideal choice for retirees looking to preserve their purchasing power.

3. Impact on Stock Market Performance

Interest rates, whether high or low, can significantly impact stock market performance. They often signal a shift toward a more cautious investment environment or stimulus for growth. A change generally impacts the stock market immediately but it may take about a year for the rest of the economy to see any widespread impact.

Stock Market Reactions:

- High Interest Rates Increase Volatility: Higher rates can make borrowing more expensive for companies, which can lead to reduced corporate profits and slower growth. Investors might sell riskier assets like stocks in favor of safer investments like bonds or savings accounts, leading to short-term market declines. Sectors like technology and real estate, which rely on cheap borrowing, are more sensitive to rate hikes. Conversely, financial stocks might benefit from rising rates as they can charge higher interest rates on loans.

- Low Interest Rates can Stimulate Growth: Lower rates can encourage investors to move money from bonds to stocks in search of higher returns, which can drive up stock prices. Low interest rates make borrowing cheaper for companies, potentially leading to increased corporate profits and expansion.

What You Can Do:

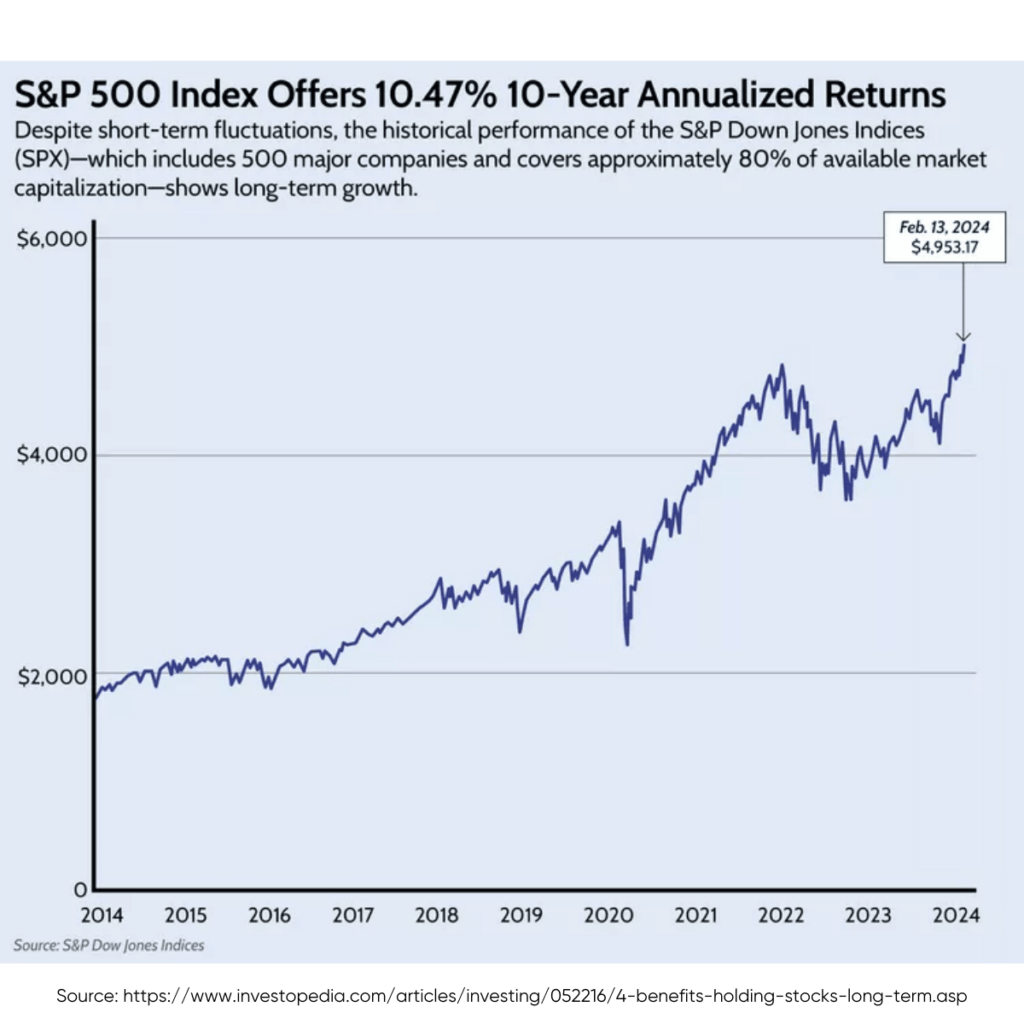

Stay Focused on Long-Term Goals: While short-term volatility can be unsettling, it’s important to stay focused on your long-term retirement goals. Trying to time the market or make drastic changes can lead to poor investment decisions. While past results are no guarantee of future returns, it does suggest that long-term investing in stocks generally yields positive results if given enough time.

Rebalance Your Portfolio: Interest rates may affect your asset allocation, so consider rebalancing your portfolio ensuring it’s aligned with your risk tolerance and time horizon.

4. Impact on Mortgage and Loan Rates

Interest rates can influence the cost of borrowing, whether you’re dealing with a mortgage, personal loan, or credit card debt. Mortgage rates are mainly influenced by the bond market, especially the yield on 10-year Treasury bonds. These yields change based on economic conditions and government policies, which in turn affect mortgage rates.

How This Affects You:

- Mortgage Rates: Rising rates increase mortgage costs, but refinancing can help if switching to a fixed-rate loan, shortening the loan term, or consolidating debt. Low rates make mortgages more affordable, offering a good opportunity to refinance and reduce monthly payments and overall interest costs.

- Credit Card Debt: Higher rates make personal loans and credit card debt more expensive, potentially straining finances, especially for retirees. On the other hand, lower rates reduce borrowing costs, making loans and credit card debt cheaper and providing an opportunity to borrow at a lower cost.

What You Can Do:

- Consider Fixed-Rate Loans: Locking in a fixed-rate mortgage before further rate hikes can help mitigate the impact of rising rates. It’s important to evaluate whether the long-term benefits outweigh any increase in monthly payments.

- Pay Off High-Interest Debt: If possible, focus on paying off any high-interest debt before retirement to reduce the financial strain. Review these four tips to pay off credit card debt faster.

5. Impact on Retirement Withdrawals

Interest rates can also affect how you manage your retirement withdrawals. If you rely on a mix of savings, investments, and bonds for your retirement income, it’s important to understand how higher rates could impact your strategy.

How This Affects You:

- High Interest Rates can Increase RMDs: If your retirement accounts are invested in bonds or interest-bearing assets, high interest rates can boost the income you generate from them. This can lead to higher Required Minimum Distributions (RMDs) when you reach age 73, providing you with more funds to manage your retirement needs. This could increase your tax liability, so plan ahead.

- Adjusting for Low Interest Rates: Lower rates might reduce the income generated from interest-bearing assets. Adjust your withdrawal strategy to ensure you don’t deplete your savings too quickly.

What You Can Do:

- Review Your Withdrawal Strategy: You may want to adjust your withdrawal strategy to account for higher income from interest-bearing assets and the potential tax implications. The Four Percent Rule has been a fundamental element in retirement planning. It’s based on the premise that retirees can safely withdraw 4.2% from their savings each year and adjust this amount by roughly 2% annually to match inflation. While the original Rule was based on the concept of “worst-case” economic scenario and stock and bond returns, some argue that 3% or 5% would be a more realistic number in today’s calculations.

- Consult a Financial Advisor: Interest rates can make retirement planning more complex, so consider working with a financial advisor to ensure your strategy is still aligned with your goals.

Navigating Interest Rates in Retirement

Interest rates present both challenges and opportunities for retirees and those saving for retirement. High rates can increase yields on savings accounts and new bonds, providing better returns for savers. However, they can also create volatility in the stock and bond markets, increase borrowing costs, and affect retirement withdrawals. On the other hand, low rates can make borrowing cheaper and boost stock market growth, but they may reduce income from interest-bearing assets.

The key to navigating this environment is diversification, a clear strategy for managing debt, and staying focused on long-term goals. By adapting to these changes and working with financial professionals, you can continue building a secure retirement despite a shifting landscape.