Growing up comes with many perks, like living life by your own rules, buying a car, getting a job, living with friends and so much more. While it’s easy to get carried away by the benefits, there are also some financial realities that young adults are faced with as they transition into adulthood.

Rising costs of living, student loans, and the growing gig economy can make it hard to get started, but establishing good financial habits early will set you up for long-term success. Here are four essential financial lessons every young person should learn:

Manage Your Money so it Doesn’t Manage You

Budgeting isn’t about restricting your lifestyle—it’s about understanding your spending habits and making sure your money works for you. Gone are the days of scribbling numbers on paper. Today, apps like Mint, YNAB (You Need A Budget), or Spendee can help automate and streamline your budgeting, making it easier than ever to track expenses, set savings goals, and see where your money goes.

**Pro Tip: Stick to the 50/30/20 rule:

- 50% of your income goes to needs (housing, groceries)

- 30% to wants (eating out, entertainment)

- 20% to savings and debt repayment

But make sure to leave room for flexibility, especially if you’re dealing with irregular income or unexpected expenses. For additional tools, check out 5 Financial Influencers on TikTok we’re following this year.

Save for a Financial Rainy Day – It Won’t Always be Sunny

The rule is simple: pay yourself first. As part of your monthly budget, put 20% of your income aside for savings and debt payoff. And while savings can apply to many things, like buying a car or taking your dream vacation, it should also apply to a rainy-day fund, also known as an emergency fund.

Life happens—whether it’s an unexpected medical bill, a job loss, or your car breaking down. An emergency fund is your financial safety net when things go wrong. Financial experts suggest saving at least three to six months of living expenses in a high-yield savings account. Set up an automatic transfer to your savings account each month. Even $50 a month adds up over time! This will not only give you peace of mind but also prevent you from resorting to high-interest debt like credit cards when life throws curveballs. Set up an automatic transfer to your savings account each month.

**Pro Tip: If you find yourself in a position where putting that much money aside is unattainable, consider these savings tips:

- 💼 Get a side job. Try Uber, DoorDash, or snag a part time job in retail or the hospitality industry.

- 📺 Cut out unnecessary expenses like audio subscriptions, streaming services, etc. Just stick to the services you use daily.

- 🌮 Cook at home! It’s oftentimes more delicious and less expensive than going out to restaurants and bars. If you really want get out, plan on going to lunch instead, split meals, use restaurant coupons, eat off the appetizer menu, and hit happy hour.

- 💳 Buy secondhand! It saves the environment and there’s no better feeling than snagging an amazing deal. Check out ThredUp, Poshmark, Facebook Marketplace, eBay, and OfferUp to get you started.

Get Smart About Debt (And Avoid Bad Habits)

Student loans, credit cards, and even buy-now-pay-later services can quickly turn into a financial mess if not managed wisely. Essentially, credit cards are a portable, plastic loan. Lenders determine how much a borrower is approved for each month, and the borrower can use it at any merchant that accepts credit. Because so many college graduates have student loan debt, taking on another form of debt, like credit, may not seem like a big deal. But it can be. Credit users may mistakenly think they have more money available than they do. Have you ever heard someone say, “I’ll just put it on my credit card”?

This thought-process can be damaging to young adults who accrue a lot of debt in a short amount of time, and the ramifications of careless spending can haunt you for a lifetime. Be sure to read the terms and understand the interest rates for any loan you take on. If you’re burdened with student loans, explore options like loan forgiveness programs or refinancing to reduce your interest rates.

**Pro Tip: Always try to pay more than the smallest amount due to save on interest. Prioritize paying off high-interest debt first (like credit cards) and focus on building a good credit score. It’ll come in handy when you need a car loan or mortgage down the road.

Start Investing for Retirement ASAP (Yes, Even in Your 20s!)

Retirement might feel like a lifetime away, but time is your biggest asset when it comes to investing. The earlier you start, the more time your money grows thanks to compound interest. If your employer offers a 401(k) plan with matching contributions, sign up immediately. If not, open a Roth IRA and set up automatic contributions to grow your retirement savings tax-free.

Consider using Robo-advisors like Bespoke if you’re new to investing—they’re beginner-friendly and can help you build a diversified portfolio.

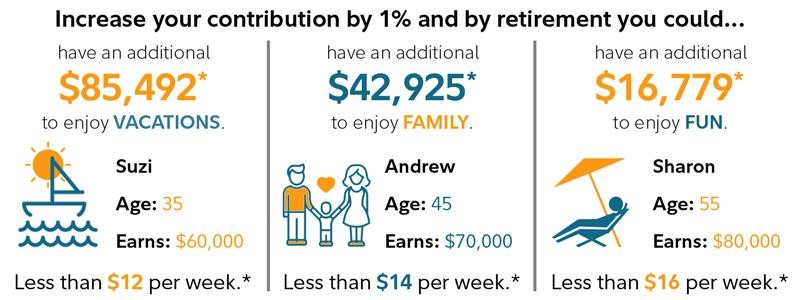

**Pro Tip: Even if your budget is tight, a 1% increase to your retirement savings each year can make a difference over the next 20 to 30 years.

Growing up comes with many perks, like living life by your own rules, buying a car, getting a job, living with friends and so much more. While it’s easy to get carried away by the benefits, there are also some financial realities that young adults are faced with as they transition into adulthood.

Source: Fidelity. * This information is intended to be educational and is not tailored to the investment needs of any specific investor.*Approximation based on a 1% increase in contribution rate. Continued employment from current age to retirement age, 67. We assume you are exactly your current age (in whole number of years) and will retire on your birthday at your retirement age. Number of years of savings equals retirement age minus current age. Nominal investment growth rate is assumed to be 5.5%. Hypothetical nominal salary growth rate is assumed to be 4% (2.5% inflation + 1.5% real salary growth rate). All accumulated retirement savings amounts are shown in future (nominal) dollars. This assumes no loans or withdrawals are taken throughout the current age to retirement age.

Remember, financial knowledge doesn’t always come easily. Sometimes it takes some research to understand how to establish your goals and manage your money As a young adult, the best thing you can do is learn how to utilize tools such as credit, budgets, retirement saving accounts, and more to avoid financial mishaps.

Read books and blogs, watch videos, and listen to podcasts to establish and maintain a strong financial foundation.