Ever thought, “I’ll get to it later,” when it comes to your finances? You’re not alone. Many of us fall into the trap of thinking there’s plenty of time to make major financial decisions. But procrastination comes with a hefty price tag—one that grows larger the longer we delay. Delaying key decisions can cost more than you imagine.

Let’s look at common areas where financial procrastination affects daily living—and more importantly, what you can do about it.

Living Paycheck to Paycheck

Not establishing a budget or an emergency fund keeps many people trapped in a cycle of living paycheck to paycheck. Without clear financial boundaries, it’s easy to overspend, under-save, and leave yourself vulnerable to unexpected expenses. A sudden car repair, medical bill, or home emergency can push you toward high-interest loans or credit card debt.

What You Can Do:

- Set up an emergency fund: Start by saving just $10 or $20 a week in a high-yield savings account. Even tiny amounts add up, and having a safety net will ease the pressure.

- Create a simple budget: Use a free app like PocketGuard or Credit Karma to track spending. You don’t need to overhaul your finances all at once. Start by setting aside 10% of your income for savings, and gradually increase it.

The “Too Little, Too Late” Effect on Health Insurance and Benefits

Procrastinating on health insurance enrollment can lead to missed savings. These accounts offer tax benefits. Delaying the use of pre-tax money for healthcare expenses means you’re paying more out of pocket. Avoiding healthcare expenses or delaying visits to doctors due to financial worries could lead to larger medical bills or health complications down the road.

What You Can Do:

- Review your health insurance: Take time during open enrollment to compare plans and ensure you are selecting one that aligns with your healthcare needs and budget.

- Utilize FSAs/HSAs: If your employer offers these accounts, contribute enough to cover expected medical expenses. These funds are tax-free and can save you hundreds annually.

Inflation and Its Erosion of Savings

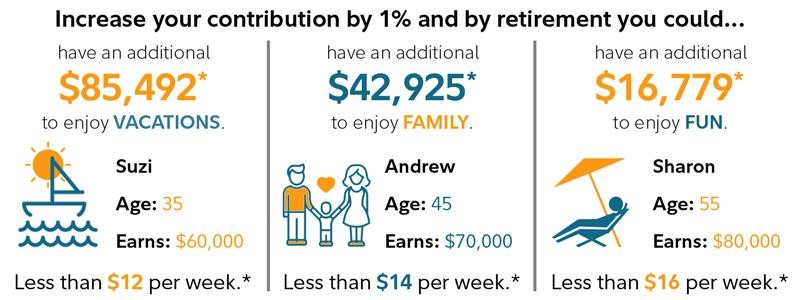

If you’re waiting to contribute to retirement plans like your 401(k) or IRA, or not contributing enough, your dreams of retiring early or taking a long-awaited vacation may be out of reach. Procrastination can significantly reduce the power of compound interest, meaning you’ll need to work longer or contribute much more later to catch up.

Waiting to invest means your cash is more likely to lose value over time due to inflation. Over decades, the purchasing power of your savings could erode, turning retirement planning into a stressful race against time. Instead of enjoying these years, you may find yourself still working or pinching pennies.

What You Can Do:

- Start contributing now: Experts often recommend investing rather than holding too much in low-interest savings accounts. If you haven’t opened a retirement account, start with a small, regular contribution —even if it’s just 1% of your income.

- Take advantage of employer matching: If your employer offers a 401(k) match, contribute enough to get the full match. This is essentially free money you’re missing if you delay.

Mounting Debt and Interest Payments

Delaying debt repayment, especially high-interest debt like credit cards, can have serious financial consequences. A $10,000 balance at a 20% interest rate can more than double if you only make minimum payments. Ignoring high-interest debt can lower your credit score.

A poor credit score means higher interest rates on loans and everyday purchases. This leads to more money spent on essentials like transportation and rent, as some landlords check credit scores. Mounting interest charges can make financial freedom harder to achieve.

What You Can Do:

- Consolidate debt and negotiate with creditors: combine high-interest debts into a single loan with a lower rate to simplify payments and reduce costs. Be sure to regularly check your credit report to catch errors and consider negotiating with creditors for lower interest rates or better repayment terms.

- Tackle debt incrementally: If you have outstanding credit card debt, start with the snowball or avalanche method to pay it down. Even paying more than the minimum each month can make a difference in the long term.

The Psychological Toll

Beyond the financial numbers, procrastination can lead to stress in all areas of your life. The longer you delay, the more you may feel overwhelmed, which makes it even harder to get started. Taking small steps now can reduce anxiety and give you a sense of control over your future.

How to Stop Procrastinating and Start Acting

- Set Small, Achievable Goals: Break large financial tasks into smaller, actionable steps. Start by setting up an automatic transfer into a retirement account each month.

- Automate Where Possible: Use automatic transfers to savings and retirement accounts. This ensures you are consistently working toward your goals without having to actively think about it each month.

- Create a Deadline: Use clear, self-imposed deadlines for financial goals. For example, “I will open an IRA by the end of the month.”

- Seek Accountability: Share your financial goals with a friend, family member, or financial advisor who can help keep you on track.

Financial procrastination is a silent but costly mistake. By understanding the true costs of delaying financial decisions, you can motivate yourself to act now. The sooner you begin tackling your financial priorities, the better positioned you’ll be for a secure and stress-free future.

{kind=link}